AML business risk assessment is considered to be the core pillar of an AML/CFT Programme. If the AML risk assessment is ineffective, the entire AML/CFT compliance framework is compromised.

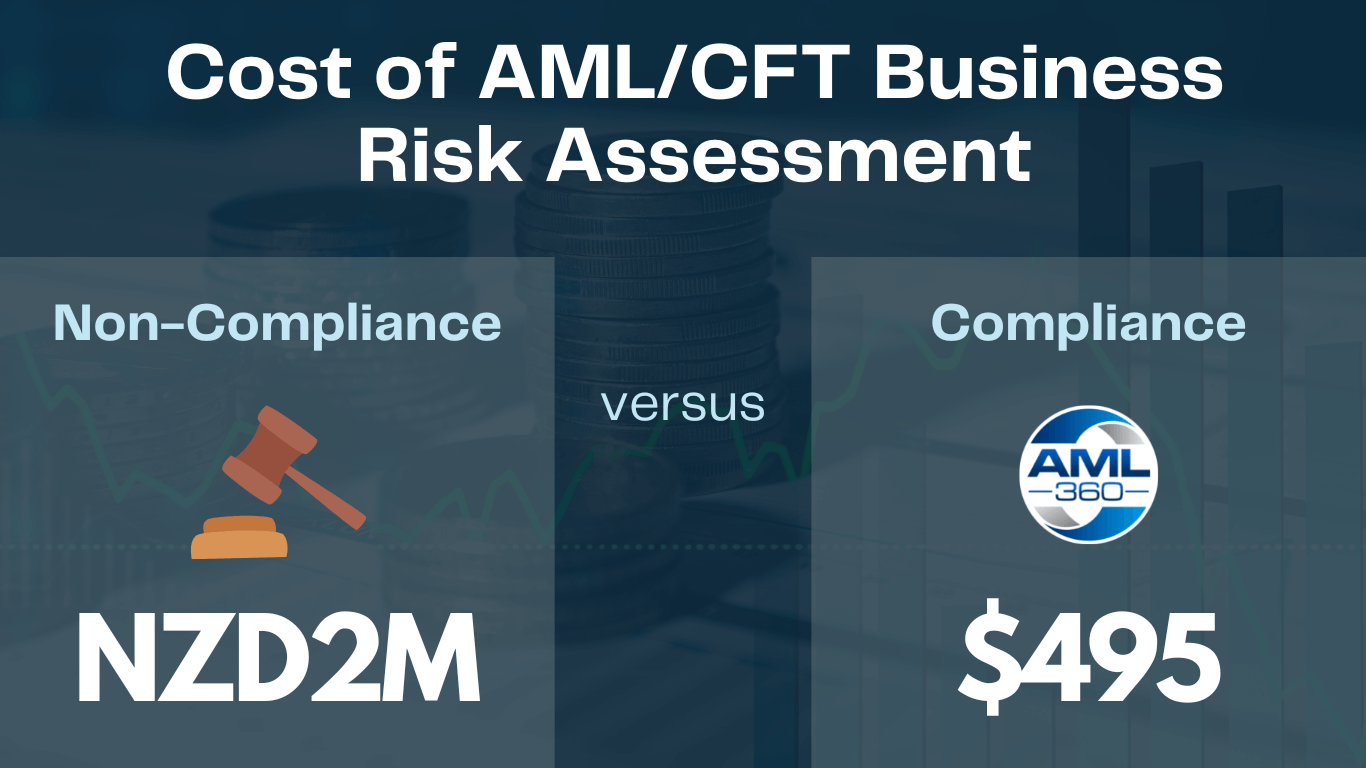

Due to the importance of an effective risk assessment, the New Zealand High Court received submissions from Government that the starting point for operating without an adequate AML/CFT business risk assessment should result in a maximum fine of $2,000,000!

The leading New Zealand case for determining pecuniary penalties for breaches of section 58 can be found in the High Court decision: Department of Internal Affairs v Qian DuoDuo Limited [2018] NZHC 1887.

In this particular case, the Crown Prosecutor guided the Court by stating:

This particular compliance failure is fundamental: the risk assessment guides a reporting entity’s business practices. If the underlying risk assessment is incorrect, then whatever practices the assessment recommends, even if those practices are in fact carried out, are unlikely to mitigate properly the risk of harm flowing from that reporting entity’s business.

CDD is a fundamental obligation under the Act – sufficiently so, that Parliament has mandated that the maximum penalty for failing to conduct CDD as required by subpart 1 of Part 2 carries a higher maximum penalty of $2 million. However, if the reporting entity’s ability to carry out the correct level of CDD obligations hinges almost entirely on undertaking the risk assessment correctly, then failure in relation to the underlying risk assessment should be seen as being equally egregious, if not more so, than compliance failures relating to CDD. Accordingly, the Department submits that, as a practical guideline, the maximum penalty for a failure to comply with s 58 should be treated in the order of $2 million.

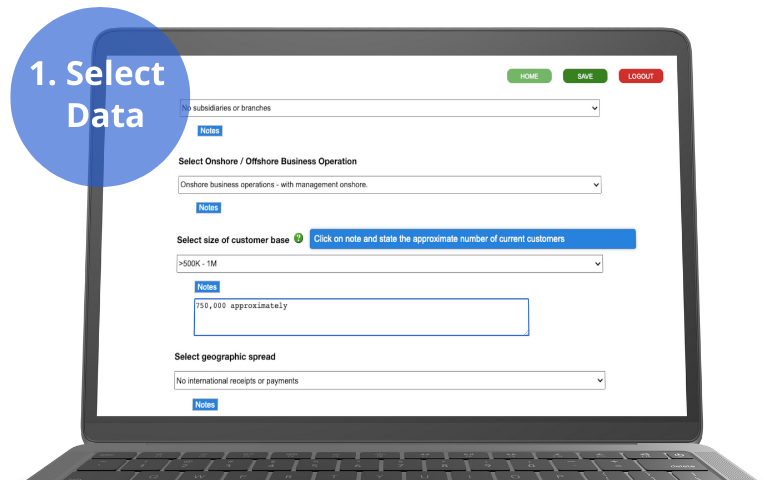

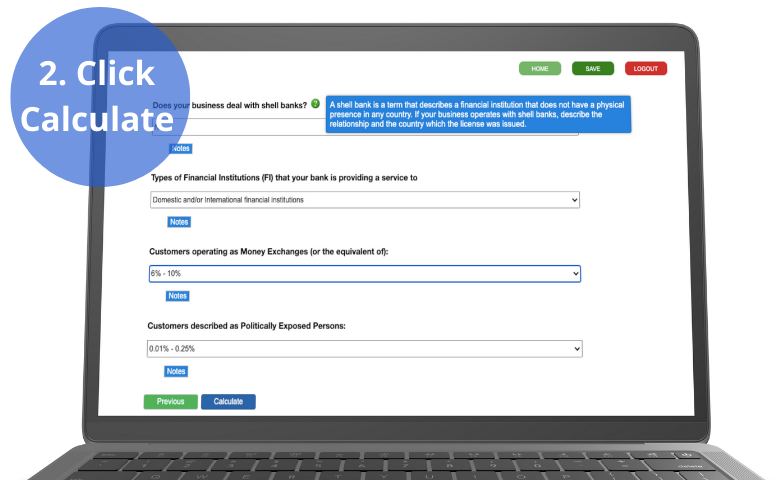

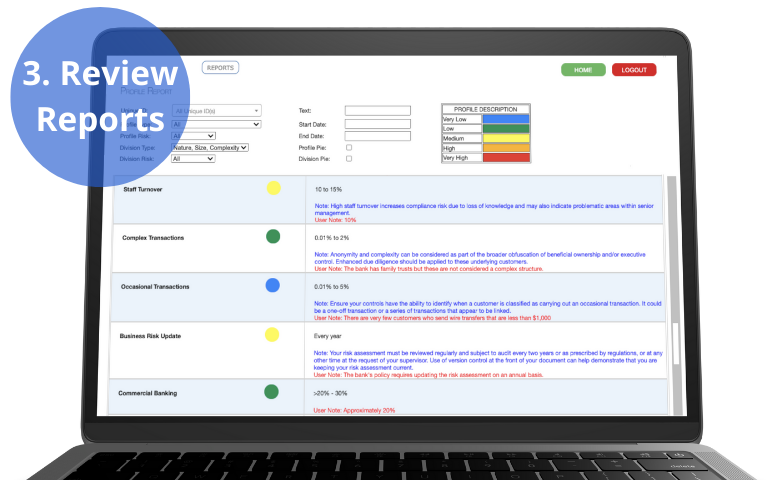

In New Zealand the obligation of conducting an AML business risk assessment arises from section 58 of the Anti-Money Laundering and Countering Financing of Terrorism Act 2009 (the AML/CFT Act). Section 58 sets out that an AML/CFT business risk assessment must include analysis of key areas of business operations that create vulnerability to facilitating money laundering and/or terrorism financing. The key areas requiring analysis are:

· The nature, size and complexity of the business

· Customers (B2B and B2C)

· Products and Services

· Method of delivering products and services

· Geographies

There are further obligations including:

· The risk assessment must be in writing; and

· Describe how the business will ensure the assessment remains current; and

· Enable the business to determine the level of risk involved in relation to relevant obligations under the AML/CFT Act and regulations.